15 Multivariate Time Series

15.1 Introduction

A multivariate time series \(Y_{t}=\left(Y_{1 t}, \ldots, Y_{m t}\right)^{\prime}\) is an \(m \times 1\) vector process observed in sequence over time, \(t=1, \ldots, n\). Multivariate time series models primarily focus on the joint modeling of the vector series \(Y_{t}\). The most common multivariate time series models used by economists are vector autoregressions (VARs). VARs were introduced to econometrics by Sims (1980).

Some excellent textbooks and review articles on multivariate time series include Hamilton (1994), Watson (1994), Canova (1995), Lütkepohl (2005), Ramey (2016), Stock and Watson (2016), and Kilian and Lütkepohl (2017).

15.2 Multiple Equation Time Series Models

To motivate vector autoregressions let us start by reviewing the autoregressive distributed lag model of Section \(14.41\) for the case of two series \(Y_{t}=\left(Y_{1 t}, Y_{2 t}\right)^{\prime}\) with a single lag. An AR-DL model for \(Y_{1 t}\) is

\[ Y_{1 t}=\alpha_{0}+\alpha_{1} Y_{1 t-1}+\beta_{1} Y_{2 t-1}+e_{1 t} . \]

Similarly, an AR-DL model for \(Y_{2 t}\) is

\[ Y_{2 t}=\gamma_{0}+\gamma_{1} Y_{2 t-1}+\delta_{1} Y_{1 t-1}+e_{2 t} . \]

These two equations specify that each variable is a linear function of its own lag and the lag of the other variable. In so doing we find that the variables on the right hand side of each equation are \(Y_{t-1}\).

We can simplify the equations by combining the regressors stacking the two equations together and writing the vector error as \(e_{t}=\left(e_{1 t}, e_{2 t}\right)^{\prime}\) to find

\[ Y_{t}=a_{0}+\boldsymbol{A}_{1} Y_{t-1}+e_{t} \]

where \(a_{0}\) is \(2 \times 1\) and \(\boldsymbol{A}_{1}\) is \(2 \times 2\). This is a bivariate vector autoregressive model for \(Y_{t}\). It specifies that the multivariate process \(Y_{t}\) is a linear function of its own lag \(Y_{t-1}\) plus \(e_{t}\). It is the combination of two equations each of which is an autoregressive distributed lag model. Thus a multivariate autoregression is a set of autoregressive distributed lag models.

The above derivation assumed a single lag. If the equations include \(p\) lags of each variable we obtain the \(p^{t h}\) order vector autoregressive (VAR) model

\[ Y_{t}=a_{0}+\boldsymbol{A}_{1} Y_{t-1}+\boldsymbol{A}_{2} Y_{t-2}+\cdots+\boldsymbol{A}_{p} Y_{t-p}+e_{t} . \]

Furthermore, there is nothing special about the two variable case. The notation in (15.1) allows \(Y_{t}=\) \(\left(Y_{1 t}, \ldots, Y_{m t}\right)^{\prime}\) to be a vector of dimension \(m\) in which case the matrices \(\boldsymbol{A}_{\ell}\) are \(m \times m\) and the error \(\boldsymbol{e}_{t}\) is \(m \times 1\). We will denote the elements of \(\boldsymbol{A}_{\ell}\) using the notation

\[ \boldsymbol{A}_{\ell}=\left[\begin{array}{cccc} a_{11, \ell} & a_{12, \ell} & \cdots & a_{1 m, \ell} \\ a_{21, \ell} & a_{22, \ell} & \cdots & a_{2 m, \ell} \\ \vdots & \vdots & & \vdots \\ a_{m 1, \ell} & a_{m 2, \ell} & \cdots & a_{m m, \ell} \end{array}\right] \]

The error \(e_{t}=\left(e_{1 t}, \ldots, e_{m t}\right)^{\prime}\) is the component of \(Y_{t}\) which is unforecastable at time \(t-1\). However, the components of \(Y_{t}\) are contemporaneously correlated. Therefore the contemporaneous covariance matrix \(\Sigma=\mathbb{E}\left[e e^{\prime}\right]\) is non-diagonal.

The VAR model falls in the class of multivariate regression models studied in Chapter 11.

In the following several sections we take a step back and provide a rigorous foundation for vector autoregressions for stationary time series.

15.3 Linear Projection

In Section \(14.14\) we derived the linear projection of the univariate series \(Y_{t}\) on its infinite past history. We now extend this to the multivariate case. Define the multivariate infinite past history \(\widetilde{Y}_{t-1}=\) \(\left(\ldots, Y_{t-2}, Y_{t-1}\right)\). The projection of \(Y_{t}\) onto \(\widetilde{Y}_{t-1}\), written \(\mathscr{P}_{t-1}\left[Y_{t}\right]=\mathscr{P}\left[Y_{t} \mid \widetilde{Y}_{t-1}\right]\), is unique and has a unique projection error

\[ e_{t}=Y_{t}-\mathscr{P}_{t-1}\left[Y_{t}\right] . \]

We will call the projection errors \(e_{t}\) the “innnovations”.

The innovations \(e_{t}\) are mean zero and serially uncorrelated. We state this formally.

Theorem 15.1 If \(Y_{t}\) is covariance stationary it has the projection equation

\[ Y_{t}=\mathscr{P}_{t-1}\left[Y_{t}\right]+e_{t} . \]

The innovations \(e_{t}\) satisfy \(\mathbb{E}\left[e_{t}\right]=0\), \(\mathbb{E}\left[e_{t-\ell} e_{t}^{\prime}\right]=0\) for \(\ell \geq 1\), and \(\Sigma=\mathbb{E}\left[e e^{\prime}\right]<\infty\). If \(Y_{t}\) is strictly stationary then \(e_{t}\) is strictly stationary.

The uncorrelatedness of the projection errors is a property of a multivariate white noise process.

Definition 15.1 The vector process \(e_{t}\) is multivariate white noise if \(\mathbb{E}\left[e_{t}\right]=0\), \(\mathbb{E}\left[e_{t} e_{t}^{\prime}\right]=\Sigma<\infty\), and \(\mathbb{E}\left[e_{t} e_{t-\ell}^{\prime}\right]=0\) for \(\ell \neq 0\)

15.4 Multivariate Wold Decomposition

By projecting \(Y_{t}\) onto the past history of the white noise innovations \(e_{t}\) we obtain a multivariate version of the Wold decomposition.

Theorem 15.2 If \(Y_{t}\) is covariance stationary and non-deterministic then it has the linear representation

\[ Y_{t}=\mu+\sum_{\ell=0}^{\infty} \Theta_{\ell} e_{t-\ell} \]

where \(e_{t}\) are the white noise projection errors and \(\Theta_{0}=\boldsymbol{I}_{m}\). The coefficient matrices \(\Theta_{\ell}\) are \(m \times m\).

We can write the moving average representation using the lag operator notation as

\[ Y_{t}=\mu+\Theta(\mathrm{L}) e_{t} \]

where

\[ \Theta(z)=\sum_{\ell=0}^{\infty} \Theta_{\ell} z^{\ell} . \]

A multivariate version of Theorem \(14.19\) can also be established.

Theorem 15.3 If \(Y_{t}\) is covariance stationary, non-deterministic, with Wold representation \(Y_{t}=\Theta(\mathrm{L}) e_{t}\), such that \(\lambda_{\min }\left(\Theta^{*}(z) \Theta(z)\right) \geq \delta>0\) for all complex \(|z| \leq 1\), and for some integer \(s \geq 0\) the Wold coefficients satisfy \(\sum_{j=0}^{\infty}\left\|\sum_{k=0}^{\infty} k^{s} \Theta_{j+k}\right\|^{2}<\infty\), then \(Y_{t}\) has an infinite-order autoregressive representation

\[ \boldsymbol{A} \text { (L) } Y_{t}=a_{0}+e_{t} \]

where

\[ \boldsymbol{A}(z)=\boldsymbol{I}_{m}-\sum_{\ell=1}^{\infty} \boldsymbol{A}_{\ell} z^{\ell} \]

and the coefficients satisfy \(\sum_{k=1}^{\infty} k^{s}\left\|\boldsymbol{A}_{k}\right\|<\infty\). The series in (15.4) is convergent.

For a proof see Section 2 of Meyer and Kreiss (2015).

We can also provide an analog of Theorem 14.6.

Theorem 15.4 If \(e_{t} \in \mathbb{R}^{m}\) is strictly stationary, ergodic, \(\mathbb{E}\left\|e_{t}\right\|<\infty\), and \(\sum_{\ell=0}^{\infty}\left\|\Theta_{\ell}\right\|<\infty\), then \(Y_{t}=\sum_{\ell=0}^{\infty} \Theta_{\ell} e_{t-\ell}\) is strictly stationary and ergodic. The proof of Theorem \(15.4\) is a straightforward extension of Theorem \(14.6\) so is omitted.

The moving average and autoregressive lag polynomials satisfy the relationship \(\Theta(z)=\boldsymbol{A}(z)^{-1}\).

For some purposes (such as impulse response calculations) we need to calculate the moving average coefficient matrices \(\Theta_{\ell}\) from the autoregressive coefficient matrices \(\boldsymbol{A}_{\ell}\). While there is not a closed-form solution there is a simple recursion by which the coefficients may be calculated.

Theorem 15.5 For \(j \geq 1, \Theta_{j}=\sum_{\ell=1}^{j} A_{\ell} \Theta_{j-\ell}\).

To see this, suppose for simplicity \(a_{0}=0\) and that the innovations satisfy \(e_{t}=0\) for \(t \neq 0\). Then \(Y_{t}=0\) for \(t<0\). Using the regression equation (15.4) for \(t \geq 0\) we solve for each \(Y_{t}\). For \(t=0\)

\[ Y_{0}=e_{0}=\Theta_{0} e_{0} \]

where \(\Theta_{0}=\boldsymbol{I}_{m}\). For \(t=1\)

\[ Y_{1}=\boldsymbol{A}_{1} Y_{0}=\boldsymbol{A}_{1} \Theta_{0} e_{0}=\Theta_{1} e_{0} \]

where \(\Theta_{1}=A_{1} \Theta_{0}\). For \(t=2\)

\[ Y_{2}=\boldsymbol{A}_{1} Y_{1}+\boldsymbol{A}_{2} Y_{0}=\boldsymbol{A}_{1} \Theta_{1} e_{0}+\boldsymbol{A}_{2} \Theta_{0} e_{0}=\Theta_{2} e_{0} \]

where \(\Theta_{2}=A_{1} \Theta_{1}+A_{2} \Theta_{0}\). For \(t=3\)

\[ Y_{3}=\boldsymbol{A}_{1} Y_{2}+\boldsymbol{A}_{2} Y_{1}+\boldsymbol{A}_{3} Y_{0}=\boldsymbol{A}_{1} \Theta_{2} e_{0}+\boldsymbol{A}_{2} \Theta_{1} e_{0}+\boldsymbol{A}_{3} \Theta_{0} e_{0}=\Theta_{3} e_{0} \]

where \(\Theta_{3}=\boldsymbol{A}_{1} \Theta_{2}+\boldsymbol{A}_{2} \Theta_{2}+\boldsymbol{A}_{2} \Theta_{0}\). The coefficients satisfy the stated recursion as claimed.

15.5 Impulse Response

One of the most important concepts in applied multivariate time series is the impulse response function (IRF) which is defined as the change in \(Y_{t}\) due to a change in an innovation or shock. In this section we define the baseline IRF - the unnormalized non-orthogonalized impulse response function - which is the change in \(Y_{t}\) due to a change in an innovation \(e_{t}\). Specifically, we define the impulse response of variable \(i\) with respect to innovation \(j\) as the change in the time \(t\) projection of the \(i^{t h}\) variable \(Y_{i t+h}\) due to the \(j^{t h}\) innovation \(e_{j t}\)

\[ \operatorname{IRF}_{i j}(h)=\frac{\partial}{\partial e_{j t}} \mathscr{P}_{t}\left[Y_{i t+h}\right] . \]

There are \(m^{2}\) such responses for each horizon \(h\). We can write them as an \(m \times m\) matrix

\[ \operatorname{IRF}(h)=\frac{\partial}{\partial e_{t}^{\prime}} \mathscr{P}_{t}\left[Y_{t+h}\right] . \]

Recall the multivariate Wold representation

\[ Y_{t}=\mu+\sum_{\ell=0}^{\infty} \Theta_{\ell} e_{t-\ell} . \]

We can calculate that the projection onto the history at time \(t\) is

\[ \mathscr{P}_{t}\left[Y_{t+h}\right]=\mu+\sum_{\ell=h}^{\infty} \Theta_{\ell} e_{t+h-\ell}=\mu+\sum_{\ell=0}^{\infty} \Theta_{h+\ell} e_{t-\ell} . \]

We deduce that the impulse response matrix is \(\operatorname{IRF}(h)=\Theta_{h}\), the \(h^{t h}\) moving average coefficient matrix. The invididual impulse response is \(\operatorname{IRF}_{i j}(h)=\Theta_{h, i j}\), the \(i j^{t h}\) element of \(\Theta_{h}\).

Here we have defined the impulse response in terms of the linear projection operator. An alternative is to define the impulse response in terms of the conditional expectation operator. The two coincide when the innovations \(e_{t}\) are a martingale difference sequence (and thus when the true process is linear) but otherwise will not coincide.

Typically we view impulse responses as a function of the horizon \(h\) and plot them as a function of \(h\) for each pair \((i, j)\). The impulse response function \(\operatorname{IRF}_{i j}(h)\) is interpreted as how the \(i^{t h}\) variable responds over time to the \(j^{t h}\) innovation.

In a linear vector autoregression the impulse response function is symmetric in negative and positive innovations. That is, the impact on \(Y_{i t+h}\) of a positive innovation \(e_{j t}=1\) is \(\operatorname{IRF}_{i j}(h)\) and the impact of a negative innovation \(e_{j t}=-1\) is \(-\operatorname{IRF}_{i j}(h)\). Furthermore, the magnitude of the impact is linear in the magnitude of the innovation. Thus the impact of the innovation \(e_{j t}=2\) is \(2 \times \operatorname{IRF}_{i j}(h)\) and the impact of the innovation \(e_{j t}=-2\) is \(-2 \times \operatorname{IRF}_{i j}(h)\). This means that the shape of the impulse response function is unaffected by the magnitude of the innovation. (These are consequences of the linearity of the vector autoregressive model, not necessarily features of the true world.)

The impulse response functions can be scaled as desired. One standard choice is to scale so that the innovations correspond to one unit of the impulse variable. Thus if the impulse variable is measured in dollars the impulse response can be scaled to correspond to a change in \(\$ 1\) or some multiple such as a million dollars. If the impulse variable is measured in percentage points (e.g. an interest rate) then the impulse response can be scaled to correspond to a change of one percentage point (e.g. from 3% to \(4 %\) ) or to correspond to a change of one basis point (e.g. from 3.05% to 3.06%). Another standard choice is to scale the impulse responses to correspond to a “one standard deviation” innovation. This occurs when the innovations have been scaled to have unit variances. In this latter case impulse response functions can be interpreted as responses due to a “typical” sized (one standard deviation) innovation.

Closely related to the IRF is the cumulative impulse response function (CIRF) defined as

\[ \operatorname{CIRF}(h)=\sum_{\ell=1}^{h} \frac{\partial}{\partial e_{t}^{\prime}} \mathscr{P}_{t}\left[Y_{t+\ell}\right]=\sum_{\ell=1}^{h} \Theta_{\ell} . \]

The cumulative impulse response is the accumulated (summed) responses on \(Y_{t}\) from time \(t\) to \(t+h\). The limit of the cumulative impulse response as \(h \rightarrow \infty\) is the long-run impulse response matrix

\[ \boldsymbol{C}=\lim _{h \rightarrow \infty} \operatorname{CIRF}(h)=\sum_{\ell=1}^{\infty} \Theta_{\ell}=\Theta(1)=\boldsymbol{A}(1)^{-1} . \]

This is the full (summed) effect of the innovation over all time.

It is useful to observe that when a VAR is estimated on differenced observations \(\Delta Y_{t}\) then cumulative impulse response is

\[ \operatorname{CIRF}(h)=\frac{\partial}{\partial e_{t}^{\prime}} \mathscr{P}_{t}\left[\sum_{\ell=1}^{h} \Delta Y_{t+\ell}\right]=\frac{\partial}{\partial e_{t}^{\prime}} \mathscr{P}_{t}\left[Y_{t+h}\right] \]

which is the impulse response for the variable \(Y_{t}\) in levels. More generally, when a VAR is estimated with some variables in levels and some in differences then the cumulative impulse response for the second group will coincide with the impulse responses for the same variables measured in levels. It is typical to report cumulative impulse response functions for variables which enter a VAR in differences. In fact, in this context many authors will label the cumulative impulse response as “the impulse response”.

15.6 VAR(1) Model

The first-order vector autoregressive process, denoted VAR(1), is

\[ Y_{t}=a_{0}+A_{1} Y_{t-1}+e_{t} \]

where \(e_{t}\) is a strictly stationary and ergodic white noise process.

We are interested in conditions under which \(Y_{t}\) is a stationary process. Let \(\lambda_{i}(\boldsymbol{A})\) denote the \(i^{\text {th }}\) eigenvalue of \(\boldsymbol{A}\).

Theorem 15.6 If \(e_{t}\) is strictly stationary, ergodic, \(\mathbb{E}\left\|e_{t}\right\|<\infty\), and \(\left|\lambda_{i}\left(A_{1}\right)\right|<1\) for \(i=1, \ldots, m\), then the \(\operatorname{VAR}(1)\) process \(Y_{t}\) is strictly stationary and ergodic.

The proof is given in Section 15.31.

15.7 \(\operatorname{VAR}(\mathrm{p})\) Model

The \(\mathbf{p}^{\text {th }}\)-order vector autoregressive process, denoted VAR(p), is

\[ Y_{t}=a_{0}+\boldsymbol{A}_{1} Y_{t-1}+\cdots+\boldsymbol{A}_{p} Y_{t-p}+e_{t} \]

where \(e_{t}\) is a strictly stationary and ergodic white noise process.

We can write the model using the lag operator notation as

\[ \boldsymbol{A} \text { (L) } Y_{t}=a_{0}+e_{t} \]

where

\[ \boldsymbol{A}(z)=\boldsymbol{I}_{m}-\boldsymbol{A}_{1} z-\cdots-\boldsymbol{A}_{p} z^{p} . \]

The condition for stationarity of the system can be expressed as a restriction on the roots of the determinantal equation of the autoregressive polynomial. Recall, a \(\operatorname{root} r\) of \(\operatorname{det}(\boldsymbol{A}(z))\) is a solution to \(\operatorname{det}(\boldsymbol{A}(r))=0\).

Theorem \(15.7\) If all roots \(r\) of \(\operatorname{det}(\boldsymbol{A}(z))\) satisfy \(|r|>1\) then the \(\operatorname{VAR}(\mathrm{p})\) process \(Y_{t}\) is strictly stationary and ergodic.

The proof is structurally identical to that of Theorem \(14.23\) so is omitted.

15.8 Regression Notation

Define the \((m p+1) \times 1\) vector

\[ X_{t}=\left(\begin{array}{c} 1 \\ Y_{t-1} \\ Y_{t-2} \\ \vdots \\ Y_{t-p} \end{array}\right) \]

and the \(m \times(m p+1)\) matrix \(\boldsymbol{A}^{\prime}=\left(\begin{array}{lllll}a_{0} & \boldsymbol{A}_{1} & \boldsymbol{A}_{2} & \cdots & \boldsymbol{A}_{p}\end{array}\right)\). Then the VAR system of equations can be written as

\[ Y_{t}=\boldsymbol{A}^{\prime} X_{t}+e_{t} . \]

This is a multivariate regression model. The error has covariance matrix

\[ \Sigma=\mathbb{E}\left[e_{t} e_{t}^{\prime}\right] . \]

We can also write the coefficient matrix as \(\boldsymbol{A}=\left(\begin{array}{llll}a_{1} & a_{2} & \cdots & a_{m}\end{array}\right)\) where \(a_{j}\) is the vector of coefficients for the \(j^{t h}\) equation. Thus \(Y_{j t}=a_{j}^{\prime} X_{t}+e_{j t}\).

In general, if \(Y_{t}\) is strictly stationary we can define the coefficient matrix \(\boldsymbol{A}\) by linear projection.

\[ \boldsymbol{A}=\left(\mathbb{E}\left[X_{t} X_{t}^{\prime}\right]\right)^{-1} \mathbb{E}\left[X_{t} Y_{t}^{\prime}\right] . \]

This holds whether or not \(Y_{t}\) is actually a \(\operatorname{VAR}(\mathrm{p})\) process. By the properties of projection errors

\[ \mathbb{E}\left[X_{t} e_{t}^{\prime}\right]=0 . \]

The projection coefficient matrix \(\boldsymbol{A}\) is identified if \(\mathbb{E}\left[X_{t} X_{t}^{\prime}\right]\) is invertible.

Theorem \(15.8\) If \(Y_{t}\) is strictly stationary and \(0<\Sigma<\infty\) for \(\Sigma\) defined in (15.6), then \(\boldsymbol{Q}=\mathbb{E}\left[X_{t} X_{t}^{\prime}\right]>0\) and the coefficient vector (14.46) is identified.

The proof is given in Section 15.31.

15.9 Estimation

From Chapter 11 the systems estimator of a multivariate regression is least squares. The estimator can be written as

\[ \widehat{\boldsymbol{A}}=\left(\sum_{t=1}^{n} X_{t} X_{t}^{\prime}\right)^{-1}\left(\sum_{t=1}^{n} X_{t} Y_{t}^{\prime}\right) . \]

Alternatively, the coefficient estimator for the \(j^{t h}\) equation is

\[ \widehat{a}_{j}=\left(\sum_{t=1}^{n} X_{t} X_{t}^{\prime}\right)^{-1}\left(\sum_{t=1}^{n} X_{t} Y_{j t}\right) . \]

The least squares residual vector is \(\widehat{e}_{t}=Y_{t}-\widehat{A}^{\prime} X_{t}\). The estimator of the covariance matrix is

\[ \widehat{\Sigma}=\frac{1}{n} \sum_{t=1}^{n} \widehat{e}_{t} \widehat{e}_{t}^{\prime} . \]

(This may be adjusted for degrees-of-freedom if desired, but there is no established finite-sample justification for a specific adjustment.)

If \(Y_{t}\) is strictly stationary and ergodic with finite variances then we can apply the Ergodic Theorem (Theorem 14.9) to deduce that

\[ \frac{1}{n} \sum_{t=1}^{n} X_{t} Y_{t}^{\prime} \underset{p}{\longrightarrow} \mathbb{E}\left[X_{t} Y_{t}^{\prime}\right] \]

and

\[ \sum_{t=1}^{n} X_{t} X_{t}^{\prime} \underset{p}{\longrightarrow} \mathbb{E}\left[X_{t} X_{t}^{\prime}\right] . \]

Since the latter is positive definite by Theorem \(15.8\) we conclude that \(\widehat{\boldsymbol{A}}\) is consistent for \(\boldsymbol{A}\). Standard manipulations show that \(\widehat{\Sigma}\) is consistent as well.

Theorem 15.9 If \(Y_{t}\) is strictly stationary, ergodic, and \(0<\Sigma<\infty\) then \(\widehat{A} \underset{p}{\rightarrow} A\) and \(\widehat{\Sigma} \underset{p}{\longrightarrow} \Sigma\) as \(n \rightarrow \infty\)

VAR models can be estimated in Stata using the var command.

15.10 Asymptotic Distribution

Set

\[ a=\operatorname{vec}(\boldsymbol{A})=\left(\begin{array}{c} a_{1} \\ \vdots \\ a_{m} \end{array}\right), \quad \widehat{a}=\operatorname{vec}(\widehat{\boldsymbol{A}})=\left(\begin{array}{c} \widehat{a}_{1} \\ \vdots \\ \widehat{a}_{m} \end{array}\right) . \]

By the same analysis as in Theorem \(14.30\) combined with Theorem \(11.1\) we obtain the following.

Theorem 15.10 Suppose that \(Y_{t}\) follows the \(\operatorname{VAR}(\mathrm{p})\) model, all roots \(r\) of \(\operatorname{det}(\boldsymbol{A}(z))\) satisfy \(|r|>1\), \(\mathbb{E}\left[e_{t} \mid \mathscr{F}_{t-1}\right]=0, \mathbb{E}\left\|e_{t}\right\|^{4}<\infty\), and \(\Sigma>0\), then as \(n \rightarrow \infty\), \(\sqrt{n}(\widehat{a}-a) \underset{d}{\longrightarrow} \mathrm{N}(0, V)\) where

\[ \begin{aligned} \boldsymbol{V} &=\overline{\boldsymbol{Q}}^{-1} \Omega \overline{\boldsymbol{Q}}^{-1} \\ \overline{\boldsymbol{Q}} &=\boldsymbol{I}_{m} \otimes \boldsymbol{Q} \\ \boldsymbol{Q} &=\mathbb{E}\left[X_{t} X_{t}^{\prime}\right] \\ \Omega &=\mathbb{E}\left[e_{t} e_{t}^{\prime} \otimes X_{t} X_{t}^{\prime}\right] . \end{aligned} \]

Notice that the theorem uses the strong assumption that the innovation is a martingale difference sequence \(\mathbb{E}\left[e_{t} \mid \mathscr{F}_{t-1}\right]=0\). This means that the \(\operatorname{VAR}(\mathrm{p})\) model is the correct conditional expectation for each variable. In words, these are the correct lags and there is no omitted nonlinearity.

If we further strengthen the MDS assumption to conditional homoskedasticity

\[ \mathbb{E}\left[e_{t} e_{t}^{\prime} \mid \mathscr{F}_{t-1}\right]=\Sigma \]

then the asymptotic variance simplifies as

\[ \begin{aligned} &\Omega=\Sigma \otimes \boldsymbol{Q} \\ &\boldsymbol{V}=\Sigma \otimes \boldsymbol{Q}^{-1} . \end{aligned} \]

In contrast, if the VAR(p) is an approximation then the MDS assumption is not appropriate. In this case the asymptotic distribution can be derived under mixing conditions.

Theorem 15.11 Assume that \(Y_{t}\) is strictly stationary, ergodic, and for some \(r>\) \(4, \mathbb{E}\left\|Y_{t}\right\|^{r}<\infty\) and the mixing coefficients satisfy \(\sum_{\ell=1}^{\infty} \alpha(\ell)^{1-4 / r}<\infty\). Let \(a\) be the projection coefficient vector and \(e_{t}\) the projection error. Then as \(n \rightarrow \infty\), \(\sqrt{n}(\widehat{a}-a) \underset{d}{\longrightarrow} \mathrm{N}(0, V)\) where

\[ \begin{aligned} &\boldsymbol{V}=\left(\boldsymbol{I}_{m} \otimes \boldsymbol{Q}^{-1}\right) \Omega\left(\boldsymbol{I}_{m} \otimes \boldsymbol{Q}^{-1}\right) \\ &\boldsymbol{Q}=\mathbb{E}\left[X_{t} X_{t}^{\prime}\right] \\ &\Omega=\sum_{\ell=-\infty}^{\infty} \mathbb{E}\left[e_{t-\ell} e_{t}^{\prime} \otimes X_{t-\ell} X_{t}^{\prime}\right] . \end{aligned} \]

This theorem does not require that the true process is a VAR. Instead, the coefficients are defined as those which produce the best (mean square) approximation, and the only requirements on the true process are general dependence conditions. The theorem shows that the coefficient estimators are asymptotically normal with a covariance matrix which takes a “long-run” sandwich form.

15.11 Covariance Matrix Estimation

The classic homoskedastic estimator of the covariance matrix for \(\widehat{a}\) equals

\[ \widehat{\boldsymbol{V}}_{\widehat{a}}^{0}=\widehat{\Sigma} \otimes\left(\boldsymbol{X}^{\prime} \boldsymbol{X}\right)^{-1} . \]

Estimators adjusted for degree-of-freedom can also be used though there is no established finite-sample justification. This variance estimator is appropriate under the assumption that the conditional expectation is correctly specified as a \(\operatorname{VAR}(\mathrm{p})\) and the innovations are conditionally homoskedastic.

The heteroskedasticity-robust estimator equals

\[ \widehat{\boldsymbol{V}}_{\widehat{a}}=\left(\boldsymbol{I}_{n} \otimes\left(\boldsymbol{X}^{\prime} \boldsymbol{X}\right)^{-1}\right)\left(\sum_{t=1}^{n}\left(\widehat{e}_{t} \widehat{e}_{t}^{\prime} \otimes X_{t} X_{t}^{\prime}\right)\right)\left(\boldsymbol{I}_{n} \otimes\left(\boldsymbol{X}^{\prime} \boldsymbol{X}\right)^{-1}\right) . \]

This variance estimator is appropriate under the assumption that the conditional expectation is correctly specified as a \(\operatorname{VAR}(\mathrm{p})\) but does not require that the innovations are conditionally homoskedastic. The Newey-West estimator equals

\[ \begin{aligned} \widehat{\boldsymbol{V}}_{\widehat{a}} &=\left(\boldsymbol{I}_{n} \otimes\left(\boldsymbol{X}^{\prime} \boldsymbol{X}\right)^{-1}\right) \widehat{\Omega}_{M}\left(\boldsymbol{I}_{n} \otimes\left(\boldsymbol{X}^{\prime} \boldsymbol{X}\right)^{-1}\right) \\ \widehat{\Omega}_{M} &=\sum_{\ell=-M}^{M} w_{\ell} \sum_{1 \leq t-\ell \leq n}\left(\widehat{e}_{t-\ell} \otimes X_{t-\ell}\right)\left(\widehat{e}_{t} \otimes X_{t}^{\prime}\right) \\ w_{\ell} &=1-\frac{|\ell|}{M+1} . \end{aligned} \]

The number \(M\) is called the lag truncation number. An unweighted version sets \(w_{\ell}=1\). The Newey-West estimator does not require that the \(\operatorname{VAR}(\mathrm{p})\) is correctly specified.

Traditional textbooks have only used the homoskedastic variance estimation formula (15.9) and consequently existing software follows the same convention. For example, the var command in Stata displays only homoskedastic standard errors. Some researchers use the heteroskedasticity-robust estimator (15.10). The Newey-West estimator (15.11) is not commonly used for VAR models.

Asymptotic approximations tend to be much less accurate under time series dependence than for independent observations. Therefore bootstrap methods are popular. In Section \(14.46\) we described several bootstrap methods for time series observations. While Section \(14.46\) focused on univariate time series, the extension to multivariate observations is straightforward.

15.12 Selection of Lag Length in an VAR

For a data-dependent rule to pick the lag length \(p\) it is recommended to minimize an information criterion. The formula for the AIC is

\[ \begin{aligned} \operatorname{AIC}(p) &=n \log \operatorname{det} \widehat{\Sigma}(p)+2 K(p) \\ \widehat{\Sigma}(p) &=\frac{1}{n} \sum_{t=1}^{n} \widehat{e}_{t}(p) \widehat{e}_{t}(p)^{\prime} \\ K(p) &=m(p m+1) \end{aligned} \]

where \(K(p)\) is the number of parameters and \(\widehat{e}_{t}(p)\) is the OLS residual vector from the model with \(p\) lags. The log determinant is the criterion from the multivariate normal likelihood.

In Stata the AIC for a set of estimated VAR models can be compared using the varsoc command. It should be noted, however, that the Stata routine actually displays \(\operatorname{AIC}(p) / n=\log \operatorname{det} \widehat{\Sigma}(p)+2 K(p) / n\). This does not affect the ranking of the models but makes the differences between models appear misleadingly small.

15.13 Illustration

We estimate a three-variable system which is a simplified version of a model often used to study the impact of monetary policy. The three variables are quarterly from FRED-QD: real GDP growth rate \(\left(100 \Delta \log \left(G D P_{t}\right)\right)\), GDP inflation rate \(\left(100 \Delta \log \left(P_{t}\right)\right)\), and the Federal funds interest rate. VARs from lags 1 through 8 were estimated by least squares. The model with the smallest AIC is the VAR(6). The coefficient estimates and (homoskedastic) standard errors for the VAR(6) are reported in Table 15.1.

Examining the coefficients in the table we can see that GDP displays a moderate degree of serial correlation and shows a large response to the federal funds rate, especially at lags 2 and 3. Inflation also displays serial correlation, shows minimal response to GDP, and also has meaningful response to the federal funds rate. The federal funds rate has the strongest serial correlation. Overall, it is difficult to read too much meaning into the coefficient estimates due to the complexity of the interactions. Because of this difficulty it is typical to focus on other representations of the coefficient estimates such as impulse responses which we discuss in the upcoming sections.

15.14 Predictive Regressions

In some contexts (including prediction) it is useful to consider models where the dependent variable is dated multiple periods ahead of the right-hand-side variables. These equations can be single equation or multivariate; we can consider both as special cases of a VAR (as a single equation model can be written as one equation taken from a VAR system). An \(h\)-step predictive VAR(p) takes the form

\[ Y_{t+h}=b_{0}+\boldsymbol{B}_{1} Y_{t}+\cdots+\boldsymbol{B}_{p} Y_{t-p+1}+u_{t} . \]

The integer \(h \geq 1\) is the horizon. A one-step predictive VAR equals a standard VAR. The coefficients should be viewed as the best linear predictors of \(Y_{t+h}\) given \(\left(Y_{t}, \ldots, Y_{t-p+1}\right)\).

There is an interesting relationship between a VAR model and the corresponding \(h\)-step predictive VAR model.

Theorem 15.12 If \(Y_{t}\) is a \(\operatorname{VAR}(\mathrm{p})\) process then its \(h\)-step predictive regression is a predictive \(\operatorname{VAR}(\mathrm{p})\) with \(u_{t}\) a MA(h-1) process and \(\boldsymbol{B}_{1}=\Theta_{h}=\operatorname{IRF}(h)\).

The proof of Theorem \(15.12\) is presented in Section 15.31.

There are several implications of this theorem. First, if \(Y_{t}\) is a \(\operatorname{VAR}(\mathrm{p})\) process then the correct number of lags for an \(h\)-step predictive regression is also \(p\) lags. Second, the error in a predictive regression is a MA process and is thus serially correlated. The linear dependence, however, is capped by the horizon. Third, the leading coefficient matrix corresponds to the \(h^{\text {th }}\) moving average coefficient matrix which also equals the \(h^{\text {th }}\) impulse response matrix.

The predictive regression (15.12) can be estimated by least squares. We can write the estimates as

\[ Y_{t+h}=\widehat{b}_{0}+\widehat{\boldsymbol{B}}_{1} Y_{t}+\cdots+\widehat{\boldsymbol{B}}_{p} Y_{t-p+1}+\widehat{u}_{t} . \]

For a distribution theory we need to apply Theorem \(15.11\) since the innovations \(u_{t}\) are a moving average and thus violate the MDS assumption. It follows as well that the covariance matrix for the estimators should be estimated by the Newey-West (15.11) estimator. There is a difference, however. Since \(u_{t}\) is known to be a MA(h-1) a reasonable choice is to set \(M=h-1\) and use the simple weights \(w_{\ell}=1\). Indeed, this was the original suggestion by L. Hansen and Hodrick (1980).

For a distributional theory we can apply Theorem 15.11. Let \(b\) be the vector of coefficients in (15.12) and \(\widehat{b}\) the corresponding least squares estimator. Let \(X_{t}\) be the vector of regressors in (15.12). Table 15.1: Vector Autoregression

| \(G D P_{t-1}\) | \(0.25\) | \(0.01\) | \(0.08\) |

|---|---|---|---|

| \((0.07)\) | \((0.02)\) | \((0.02)\) | |

| \(G D P_{t-2}\) | \(0.23\) | \(-0.02\) | \(0.04\) |

| \((0.07)\) | \((0.02)\) | \((0.02)\) | |

| \(G D P_{t-3}\) | \(0.00\) | \(0.03\) | \(0.01\) |

| \((0.07)\) | \((0.02)\) | \((0.02)\) | |

| \(G D P_{t-4}\) | \(0.14\) | \(0.04\) | \(-0.02\) |

| \((0.07)\) | \((0.02)\) | \((0.02)\) | |

| \(G D P_{t-5}\) | \(-0.02\) | \(-0.03\) | \(0.04\) |

| \((0.07)\) | \((0.02)\) | \((0.02)\) | |

| \(G D P_{t-6}\) | \(0.05\) | \(-0.00\) | \(-0.01\) |

| \((0.06)\) | \((0.02)\) | \((0.02)\) | |

| \(I N F_{t-1}\) | \(0.11\) | \(0.57\) | \(0.01\) |

| \((0.20)\) | \((0.07)\) | \((0.05)\) | |

| \(I N F_{t-2}\) | \(-0.17\) | \(0.10\) | \(0.17\) |

| \((0.23)\) | \((0.08)\) | \((0.06)\) | |

| \(I N F_{t-3}\) | \(0.01\) | \(0.09\) | \(-0.05\) |

| \((0.23)\) | \((0.08)\) | \((0.06)\) | |

| \(I N F_{t-4}\) | \(0.16\) | \(0.14\) | \(-0.05\) |

| \((0.23)\) | \((0.08)\) | \((0.06)\) | |

| \(I N F_{t-5}\) | \(0.12\) | \(-0.05\) | \(-0.05\) |

| \((0.24)\) | \((0.08)\) | \((0.06)\) | |

| \(I N F_{t-6}\) | \(-0.14\) | \(0.10\) | \(0.09\) |

| \((0.21)\) | \((0.07)\) | \((0.05)\) | |

| \(F F_{t-1}\) | \(0.13\) | \(0.28\) | \(1.14\) |

| \((0.26)\) | \((0.08)\) | \((0.07)\) | |

| \(F F_{t-2}\) | \(-1.50\) | \(-0.27\) | \(-0.53\) |

| \((0.38)\) | \((0.12)\) | \((0.10)\) | |

| \(F F_{t-3}\) | \(1.40\) | \(0.12\) | \(0.53\) |

| \((0.40)\) | \((0.13)\) | \((0.10)\) | |

| \(F F_{t-4}\) | \(-0.57\) | \(-0.13\) | \(-0.28\) |

| \((0.41)\) | \((0.13)\) | \((0.11)\) | |

| \(0.01\) | \(0.25\) | \(0.28\) | |

| \((0.40)\) | \((0.13)\) | \((0.10)\) | |

| \(-0.27\) | \(-0.24\) | ||

| \((0.18)\) | \((0.14)\) |

Theorem 15.13 If \(Y_{t}\) is strictly stationary, ergodic, \(\Sigma>0\), and for some \(r>4\), \(\mathbb{E}\left\|Y_{t}\right\|^{r}<\infty\) and the mixing coefficients satisfy \(\sum_{\ell=1}^{\infty} \alpha(\ell)^{1-4 / r}<\infty\), then as \(n \rightarrow\) \(\infty, \sqrt{n}(\widehat{b}-b) \underset{d}{\longrightarrow} \mathrm{N}(0, V)\) where

\[ \begin{aligned} \boldsymbol{V} &=\left(\boldsymbol{I}_{m} \otimes \boldsymbol{Q}^{-1}\right) \Omega\left(\boldsymbol{I}_{m} \otimes \boldsymbol{Q}^{-1}\right) \\ \boldsymbol{Q} &=\mathbb{E}\left[X_{t} X_{t}^{\prime}\right] \\ \Omega &=\sum_{\ell=-\infty}^{\infty} \mathbb{E}\left[\left(\widehat{u}_{t-\ell} \otimes X_{t-\ell}\right)\left(\widehat{u}_{t}^{\prime} \otimes X_{t}^{\prime}\right)\right] . \end{aligned} \]

15.15 Impulse Response Estimation

Reporting of impulse response estimates is one of the most common applications of vector autoregressive modeling. There are several methods to estimate the impulse response function. In this section we review the most common estimator based on the estimated VAR parameters.

Within a VAR(p) model the impulse responses are determined by the VAR coefficients. We can write this mapping as \(\Theta_{h}=g_{h}(\boldsymbol{A})\). The plug-in approach suggests the estimator \(\widehat{\Theta}_{h}=g_{h}(\widehat{\boldsymbol{A}})\) given the \(\operatorname{VAR}(\mathrm{p})\) coefficient estimator \(\widehat{A}\). These are the impulse responses implied by the estimated VAR coefficients. While it is possible to explicitly write the function \(g_{h}(\boldsymbol{A})\), a computationally simple approach is to use Theorem \(15.5\) which shows that the impulse response matrices can be written as a simple recursion in the VAR coefficients. Thus the impulse response estimator satisfies the recursion

\[ \widehat{\Theta}_{h}=\sum_{\ell=1}^{\min [h, p]} \widehat{A}_{\ell} \widehat{\Theta}_{h-\ell} . \]

We then set \(\widehat{\operatorname{IRF}}(h)=\widehat{\Theta}_{h}\).

This is the the most commonly used method for impulse response estimation and it is the method implemented in standard packages.

Since \(\widehat{A}\) is random so is \(\widehat{\operatorname{IRF}}(h)\) as it is a nonlinear function of \(\widehat{\boldsymbol{A}}\). Using the delta method, we deduce that the elements of \(\widehat{\operatorname{IRF}}(h)\) (the impulse responses) are asymptotically normally distributed. With some messy algebra explicit expressions for the asymptotic variances can be obtained. Sample versions can be used to calculate asymptotic standard errors. These can be used to form asymptotic confidence intervals for the impulse responses.

The asymptotic approximations, however, can be poor. As we discussed earlier the asymptotic approximations for the distribution of the coefficients \(\widehat{A}\) can be poor due to the serial dependence in the observations. The asymptotic approximations for \(\widehat{\operatorname{IRF}}(h)\) can be significantly worse because the impulse responses are highly nonlinear functions of the coefficients. For example, in the simple AR(1) model with coefficient estimate \(\widehat{\alpha}\) the \(h^{\text {th }}\) impulse response is \(\widehat{\alpha}^{h}\) which is highly nonlinear for even moderate horizons \(h\).

Consequently, asymptotic approximations are less popular than bootstrap approximations. The most popular bootstrap approximation uses the recursive bootstrap (see Section 14.46) using the fitted VAR model and calculates confidence intervals for the impulse responses with the percentile method. An unfortunate feature of this choice is that the percentile bootstrap confidence interval is biased since the nonlinear impulse response estimates are biased and the percentile bootstrap accentuates bias. Some advantages of the estimation method as described is that it produces impulse response estimates which are directly related to the estimated \(\operatorname{VAR}(\mathrm{p})\) model and are internally consistent with one another. The method is also numerically stable. It is efficient when the true process is a true \(\operatorname{VAR}(\mathrm{p})\) with conditionally homoskedastic MDS innovations. When the true process is not a VAR(p) it can be thought of as a nonparametric estimator of the impulse response if \(p\) is large (or selected appropriately in a data-dependent fashion, such as by the AIC).

A disadvantage of this estimator is that it is a highly nonlinear function of the VAR coefficient estimators. Therefore the distribution of the impulse response estimator is unlikely to be well approximated by the normal distribution. When the \(\operatorname{VAR}(\mathrm{p})\) is not the true process then it is possible that the nonlinear transformation accentuates the misspecification bias.

Impulse response functions can be calculated and displayed in Stata using the irf command. The command irf create is used to calculate impulse response functions and confidence intervals. The default confidence intervals are asymptotic (delta method). Bootstrap (recursive method) standard errors can be substituted using the bs option. The command irf graph irf produces graphs of the impulse response function along with \(95 %\) asymptotic confidence intervals. The command irf graph cirf produces the cumulative impulse response function. It may be useful to know that the impulse response estimates are unscaled so represent the response due to a one-unit change in the impulse variable. A limitation of the Stata irf command is that there are limited options for standard error and confidence interval construction. The asymptotic standard errors are calculated using the homoskedastic formula not the correct heteroskedastic formula. The bootstrap confidence intervals are calculated using the normal approximation bootstrap confidence interval, the least reliable bootstrap confidence interval method. Better options such as the bias-corrected percentile confidence interval are not provided as options.

15.16 Local Projection Estimator

Jordà (2005) observed that the impulse response can be estimated by a least squares predictive regression. The key is Theorem \(15.12\) which established that \(\Theta_{h}=\boldsymbol{B}_{1}\), the leading coefficient matrix in the \(h\)-step predictive regression.

The method is as follows. For each horizon \(h\) estimate a predictive regression (15.12) to obtain the leading coefficient matrix estimator \(\widehat{\boldsymbol{B}}_{1}\). The estimator is \(\widehat{\operatorname{IRF}}(h)=\widehat{\boldsymbol{B}}_{1}\) and is known as the local projection estimator.

Theorem \(15.13\) shows that the local projection impulse response estimator is asymptotically normal. Newey-West methods must be used for calculation of asymptotic standard errors since the regression errors are serially correlated.

Jordà (2005) speculates that the local projection estimator will be less sensitive to misspecification since it is a straightforward linear estimator. This is intuitive but unclear. Theorem \(15.12\) relies on the assumption that \(Y_{t}\) is a \(\operatorname{VAR}(\mathrm{p})\) process, and fails otherwise. Thus if the true process is not a VAR(p) then the coefficient matrix \(\boldsymbol{B}_{1}\) in (15.12) does not correspond to the desired impulse response matrix \(\Theta_{h}\) and hence will be misspecified. The accuracy (in the sense of low bias) of both the conventional and the local projection estimator relies on \(p\) being sufficiently large that the \(\operatorname{VAR}(\mathrm{p})\) model is a good approximation to the true infinite-order regression (15.4). Without a formal theory it is difficult to know which estimator is more robust than the other.

One implementation challenge is the choice of \(p\). While the method allows for \(p\) to vary across horizon \(h\) there is no well-established method for selection of the VAR order for predictive regressions. (Standard selection criteria such as AIC are inappropriate under serially correlated errors just as conventional standard errors are inappropriate.) Therefore the seemingly natural choice is to use the same \(p\) for all horizons and base this choice on the one-step VAR model where AIC can be used for model selection.

An advantage of the local projection method is that it is a linear estimator of the impulse response and thus likely to have a better-behaved sampling distribution.

A disadvantage is that the method relies on a regression (15.12) that has serially correlated errors. The latter are highly correlated at long horizons and this renders the estimator imprecise. Local projection estimators tend to be less smooth and more erratic than those produced by the conventional estimator reflecting a possible lack of precision.

15.17 Regression on Residuals

If the innovations \(e_{t}\) were observed it would be natural to directly estimate the coefficients of the multivariate Wold decomposition. We would pick a maximum horizon \(h\) and then estimate the equation

\[ Y_{t}=\mu+\Theta_{1} e_{t-1}+\Theta_{2} e_{t-2}+\cdots+\Theta_{h} e_{t-h}+u_{t} \]

where

\[ u_{t}=e_{t}+\sum_{\ell=h+1}^{\infty} \Theta_{\ell} e_{t-\ell} . \]

The variables \(\left(e_{t-1}, \ldots, e_{t-h}\right)\) are uncorrelated with \(u_{t}\) so the least squares estimator of the coefficients is consistent and asymptotically normal. Since \(u_{t}\) is serially correlated the Newey-West method should be used to calculate standard errors.

In practice the innovations \(e_{t}\) are not observed. If they are replaced by the residuals \(\widehat{e}_{t}\) from an estimated \(\operatorname{VAR}(\mathrm{p})\) then we can estimate the coefficients by least squares applied to the equation

\[ Y_{t}=\mu+\Theta_{1} \widehat{e}_{t-1}+\Theta_{2} \widehat{e}_{t-2}+\cdots+\Theta_{h} \widehat{e}_{t-h}+\widehat{u}_{t} . \]

This idea originated with Durbin (1960).

This is a two-step estimator with generated regressors. (See Section 12.26.) The impulse response estimators are consistent and asymptotically normal but with a non-standard covariance matrix due to the two-step estimation. Conventional, robust, and Newey-West standard errors do not account for this without modification.

Chang and Sakata (2007) proposed a simplified version of the Durbin regression. Notice that for any horizon \(h\) we can rewrite the Wold decomposition as

\[ Y_{t+h}=\mu+\Theta_{h} e_{t}+v_{t+h} \]

where

\[ v_{t}=\sum_{\ell=0}^{h-1} \Theta_{\ell} e_{t-\ell}+\sum_{\ell=h+1}^{\infty} \Theta_{\ell} e_{t-\ell} . \]

The regressor \(e_{t}\) is uncorrelated with \(v_{t+h}\). Thus \(\Theta_{h}\) can be estimated by a regression of \(Y_{t+h}\) on \(e_{t}\). In practice we can replace \(e_{t}\) by the least squares residual \(\widehat{e}_{t}\) from an estimated VAR(p) to estimate the regression

\[ Y_{t+h}=\mu+\Theta_{h} \widehat{e}_{t}+\widehat{v}_{t+h} . \]

Similar to the Durbin regression the Chang-Sakata estimator is a two-step estimator with a generated regressor. However, as it takes the form studied in Section \(12.27\) it can be shown that the Chang-Sakata two-step estimator has the same asymptotic distribution as the idealized one-step estimator as if \(e_{t}\) were observed. Thus the standard errors do not need to be adjusted for generated regressors which is an advantage. The errors are serially correlated so Newey-West standard errors should be used. The variance of the error \(v_{t+h}\) is larger than the variance of the error \(u_{t}\) in the Durbin regression so the Chang-Sakata estimator may be less precise than the Durbin estimator.

Chang and Sakata (2007) also point out the following implication of the FWL theorem. The least squares slope estimator in (15.14) is algebraically identical \({ }^{1}\) to the slope estimator \(\widehat{\boldsymbol{B}}_{1}\) in a predictive regression with \(p-1\) lags. Thus the Chang-Sakata estimator is similar to a local projection estimator.

15.18 Orthogonalized Shocks

We can use the impulse response function to examine how the innnovations impact the time-paths of the variables. A difficulty in interpretation, however, is that the elements of the innovation vector \(e_{t}\) are contemporeneously correlated. Thus \(e_{j t}\) and \(e_{i t}\) are (in general) not independent, so consequently it does not make sense to treat \(e_{j t}\) and \(e_{i t}\) as fundamental “shocks”. Another way of describing the problem is that it does not make sense, for example, to describe the impact of \(e_{j t}\) while “holding” \(e_{i t}\) constant.

The natural solution is to orthogonalize the innovations so that they are uncorrelated and then view the orthogonalized errors as the fundamental “shocks”. Recall that \(e_{t}\) is mean zero with covariance matrix \(\Sigma\). We can factor \(\Sigma\) into the product of an \(m \times m\) matrix \(\boldsymbol{B}\) with its transpose \(\Sigma=\boldsymbol{B} \boldsymbol{B}^{\prime}\). The matrix \(\boldsymbol{B}\) is called a “square root” of \(\Sigma\). (See Section A.13.) Define \(\varepsilon_{t}=\boldsymbol{B}^{-1} e_{t}\). The random vector \(\varepsilon_{t}\) has mean zero and covariance matrix \(\boldsymbol{B}^{-1} \Sigma \boldsymbol{B}^{-1 \prime}=\boldsymbol{B}^{-1} \boldsymbol{B} \boldsymbol{B}^{\prime} \boldsymbol{B}^{-1 \prime}=\boldsymbol{I}_{m}\). The elements \(\varepsilon_{t}=\left(\varepsilon_{1 t}, \ldots, \varepsilon_{m t}\right)\) are mutually uncorrelated. We can write the innovations as a function of the orthogonalized errors as

\[ e_{t}=\boldsymbol{B} \varepsilon_{t} . \]

To distinguish \(\varepsilon_{t}\) from \(e_{t}\) we will typically call \(\varepsilon_{t}\) the “orthogonalized shocks” or more simply as the “shocks” and continue to call \(e_{t}\) the “innovations”.

When \(m>1\) there is not a unique square root matrix \(\boldsymbol{B}\) so there is not a unique orthogonalization. The most common choice (and was originally advocated by Sims (1980)) is the Cholesky decomposition (see Section A.16). This sets \(\boldsymbol{B}\) to be lower triangular, meaning that it takes the form

\[ \boldsymbol{B}=\left[\begin{array}{ccc} b_{11} & 0 & 0 \\ b_{21} & b_{22} & 0 \\ b_{31} & b_{32} & b_{33} \end{array}\right] \]

with non-negative diagonal elements. We can write the Cholesky decomposition of a matrix \(\boldsymbol{A}\) as \(\boldsymbol{C}=\) \(\operatorname{chol}(\boldsymbol{A})\) which means that \(\boldsymbol{A}=\boldsymbol{C} \boldsymbol{C}^{\prime}\) with \(\boldsymbol{C}\) lower triangular. We thus set

\[ \boldsymbol{B}=\operatorname{chol}(\Sigma) \]

Equivalently, the innovations are related to the orthogonalized shocks by the equations

\[ \begin{aligned} &e_{1 t}=b_{11} \varepsilon_{1 t} \\ &e_{2 t}=b_{21} \varepsilon_{1 t}+b_{22} \varepsilon_{2 t} \\ &e_{3 t}=b_{31} \varepsilon_{1 t}+b_{31} \varepsilon_{2 t}+b_{33} \varepsilon_{3 t} . \end{aligned} \]

This structure is recursive. The innovation \(e_{1 t}\) is a function only of the single shock \(\varepsilon_{1 t}\). The innovation \(e_{2 t}\) is a function of the shocks \(\varepsilon_{1 t}\) and \(\varepsilon_{2 t}\), and the innovation \(e_{3 t}\) is a function of all three shocks. Another way of looking at the structure is that the first shock \(\varepsilon_{1 t}\) affects all three innovationa, the second shock \(\varepsilon_{2 t}\) affects \(e_{2 t}\) and \(e_{3 t}\), and the third shock \(\varepsilon_{3 t}\) only affects \(e_{3 t}\).

\({ }^{1}\) Technically, if the sample lengths are adjusted. A recursive structure is an exclusion restriction. The recursive structure excludes \(\varepsilon_{2 t}\) and \(\varepsilon_{3 t}\) contemporeneously affecting \(e_{1 t}\), and excludes \(\varepsilon_{3 t}\) contemporeneously affecting \(e_{2 t}\).

When using the Cholesky decomposition the recursive structure is determined by the ordering of the variables in the system. The order matters and is the key identifying assumption. We will return to this issue later.

Finally, we mention that the system (15.15) is equivalent to the system

\[ A e_{t}=\varepsilon_{t} \]

where \(\boldsymbol{A}=\boldsymbol{B}^{-1}\) is lower triangular when \(\boldsymbol{B}\) is lower triangular. The representation (15.15) is more convenient, however, for most of our purposes.

15.19 Orthogonalized Impulse Response Function

We have defined the impulse response function as the change in the time \(t\) projection of the variables \(Y_{t+h}\) due to the innovation \(e_{t}\). As we discussed in the previous section, since the innovations are contemporeneously correlated it makes better sense to focus on changes due to the orthogonalized shocks \(\varepsilon_{t}\). Consequently we define the orthgonalized impulse response function (OIRF) as

\[ \operatorname{OIRF}(h)=\frac{\partial}{\partial \varepsilon_{t}^{\prime}} \mathscr{P}_{t}\left[Y_{t+h}\right] . \]

We can write the multivariate Wold representation as

\[ Y_{t}=\mu+\sum_{\ell=0}^{\infty} \Theta_{\ell} e_{t-\ell}=\mu+\sum_{\ell=0}^{\infty} \Theta_{\ell} \boldsymbol{B} \varepsilon_{t-\ell} \]

where \(\boldsymbol{B}\) is from (15.16). We deduce that

\[ \operatorname{OIRF}(h)=\Theta_{h} \boldsymbol{B}=\operatorname{IRF}(h) \boldsymbol{B} . \]

This is the non-orthogonalized impulse response matrix multiplied by the matrix square root \(\boldsymbol{B}\).

Write the rows of the matrix \(\Theta_{h}\) as

\[ \Theta_{h}=\left[\begin{array}{c} \theta_{1 h}^{\prime} \\ \theta_{m h}^{\prime} \end{array}\right] \]

and the columns of the matrix \(\boldsymbol{B}\) as \(\boldsymbol{B}=\left[b_{1}, \ldots, b_{m}\right]\). We can see that

\[ \operatorname{OIRF}_{i j}(h)=\left[\Theta_{h} \boldsymbol{B}\right]_{i j}=\theta_{i h}^{\prime} b_{j} . \]

There are \(m^{2}\) such responses for each horizon \(h\).

The cumulative orthogonalized impulse response function (COIRF) is

\[ \operatorname{COIRF}(h)=\sum_{\ell=1}^{h} \operatorname{OIRF}(\ell)=\sum_{\ell=1}^{h} \Theta_{\ell} \boldsymbol{B} \]

15.20 Orthogonalized Impulse Response Estimation

We have discussed estimation of the moving average matrices \(\Theta_{\ell}\). We need an estimator of \(\boldsymbol{B}\).

We first estimate the VAR(p) model by least squares. This gives us the coefficient matrices \(\widehat{A}\) and the error covariance matrix \(\widehat{\Sigma}\). From the latter we apply the Cholesky decomposition \(\widehat{\boldsymbol{B}}=\operatorname{chol}(\widehat{\Sigma})\) so that \(\widehat{\Sigma}=\widehat{\boldsymbol{B}} \widehat{\boldsymbol{B}}^{\prime}\). (See Section A.16 for the algorithm.) The orthogonalized impulse response estimators are

\[ \widehat{\operatorname{OIRF}}(h)=\widehat{\Theta}_{h} \widehat{\boldsymbol{B}}=\widehat{\theta}_{i h}^{\prime} \widehat{b}_{j} . \]

The estimator \(\widehat{\mathrm{OIRF}}(h)\) is a nonlinear function of \(\widehat{\boldsymbol{A}}\) and \(\widehat{\Sigma}\). It is asymptotically normally distributed by the delta method. This allows for explicit calculation of asymptotic standard errors. These can be used to form asymptotic confidence intervals for the impulse responses.

As discussed earlier, the asymptotic approximations can be quite poor. Consequently bootstrap approximations are more widely used than asymptotic methods.

Orthogonalized impulse response functions can be displayed in Stata using the irf command. The command irf graph oirf produces graphs of the orthogonalized impulse response function along with \(95 %\) asymptotic confidence intervals. The command irf graph coirf produces the cumulative orthogonalized impulse response function. It may also be useful to know that the OIRF are scaled for a one-standard deviation shock so the impulse response represents the response due to a one-standarddeviation change in the impulse variable. As discussed earlier, the Stata irf command has limited options for standard error and confidence interval construction. The asymptotic standard errors are calculated using the homoskedastic formula not the correct heteroskedastic formula. The bootstrap confidence intervals are calculated using the normal approximation bootstrap confidence interval.

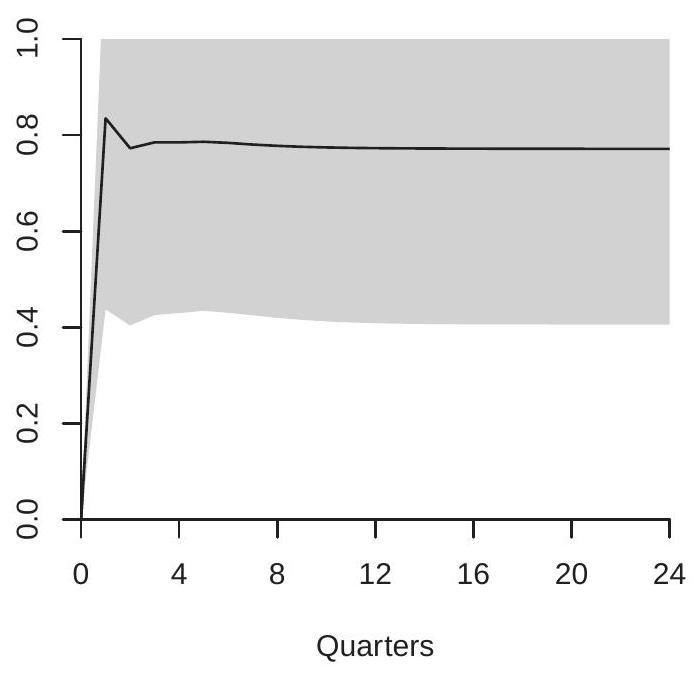

15.21 Illustration

To illustrate we use the three-variable system from Section 15.13. We use the ordering (1) real GDP growth rate, (2) inflation rate, (3) Federal funds interest rate. We discuss the choice later when we discuss identification. We use the estimated VAR(6) and calculate the orthogonalized impulse response functions using the standard VAR estimator.

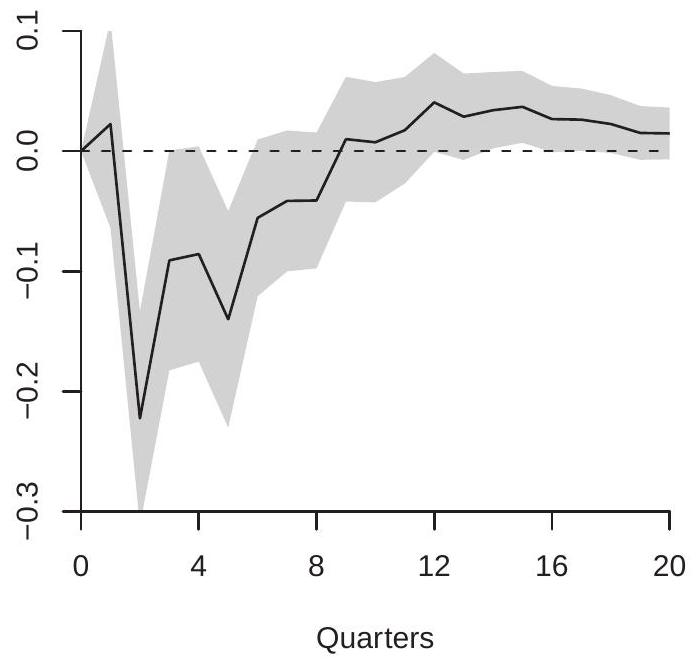

In Figure \(15.1\) we display the estimated orthogonalized impulse response of the GDP growth rate in response to a one standard deviation increase in the federal funds rate. Panel (a) shows the impulse response function and panel (b) the cumulative impulse response function. As we discussed earlier the interpretation of the impulse response and the cumulative impulse response depends on whether the variable enters the VAR in differences or in levels. In this case, GDP growth is the first difference of the natural logarithm. Thus panel (a) (the impulse response function) shows the effect of interest rates on the growth rate of GDP. Panel (b) (the cumulative impulse response) shows the effect on the log-level of GDP. The IRF shows that the GDP growth rate is negatively affected in the second quarter after an interest rate increase (a drop of about \(0.2 %\), non-annualized), and the negative effects continue for several quarters following. The CIRF shows the effect on the level of GDP measured as percentage changes. It shows that an interest rate increase causes GDP to fall for about 8 quarters, reducing GDP by about \(0.6 %\).

15.22 Forecast Error Decomposition

An alternative tool to investigate an estimated VAR is the forecast error decomposition which decomposes multi-step forecast error variances by the component shocks. The forecast error decomposition indicates which shocks contribute towards the fluctuations of each variable in the system.

- Impulse Response Function

.jpg)

- Cumulative IRF

Figure 15.1: Response of GDP Growth to Orthogonalized Fed Funds Shock

It is defined as follows. Take the moving average representation of the \(i^{\text {th }}\) variable \(Y_{i, t+h}\) written as a function of the orthogonalized shocks

\[ Y_{i, t+h}=\mu_{i}+\sum_{\ell=0}^{\infty} \theta_{i}(\ell)^{\prime} \boldsymbol{B} \varepsilon_{t+h-\ell} . \]

The best linear forecast of \(Y_{t+h}\) at time \(t\) is

\[ Y_{i, t+h \mid t}=\mu_{i}+\sum_{\ell=h}^{\infty} \theta_{i}(\ell)^{\prime} \boldsymbol{B} \varepsilon_{t+h-\ell} . \]

The \(h\)-step forecast error is the difference

\[ Y_{i, t+h}-Y_{i, t+h \mid t}=\sum_{\ell=0}^{h-1} \theta_{i}(\ell)^{\prime} \boldsymbol{B} \varepsilon_{t+h-\ell} . \]

The variance of this forecast error is

\[ \operatorname{var}\left[Y_{i, t+h}-Y_{i, t+h \mid t}\right]=\sum_{\ell=0}^{h-1} \operatorname{var}\left[\theta_{i}(\ell)^{\prime} \boldsymbol{B} \varepsilon_{t+h-\ell}\right]=\sum_{\ell=0}^{h-1} \theta_{i}(\ell)^{\prime} \boldsymbol{B} \boldsymbol{B}^{\prime} \theta_{i}(\ell) . \]

To isolate the contribution of the \(j^{t h}\) shock, notice that

\[ e_{t}=\boldsymbol{B} \varepsilon_{t}=b_{1} \varepsilon_{1 t}+\cdots+b_{m} \varepsilon_{m t} . \]

Thus the contribution of the \(j^{t h}\) shock is \(b_{j} \varepsilon_{j t}\). Now imagine replacing \(\boldsymbol{B} \varepsilon_{t}\) in the variance calculation by the \(j^{t h}\) contribution \(b_{j} \varepsilon_{j t}\). This is

\[ \operatorname{var}\left[Y_{i t+h}-Y_{i, t+h \mid t}\right]=\sum_{\ell=0}^{h-1} \operatorname{var}\left[\theta_{i}(\ell)^{\prime} b_{j} \varepsilon_{j t+h-\ell}\right]=\sum_{\ell=0}^{h-1}\left(\theta_{i}(\ell)^{\prime} b_{j}\right)^{2} . \]

Examining (15.18) and using \(\boldsymbol{B}=\left[b_{1}, \ldots, b_{m}\right]\) we can write (15.18) as

\[ \operatorname{var}\left[Y_{i, t+h}-Y_{i, t+h \mid t}\right]=\sum_{j=1}^{m} \sum_{\ell=0}^{h-1}\left(\theta_{i}(\ell)^{\prime} b_{j}\right)^{2} . \]

The forecast error decomposition is defined as the ratio of the \(j^{t h}\) contribution to the total which is the ratio of (15.19) to (15.20):

\[ \mathrm{FE}_{i j}(h)=\frac{\sum_{\ell=0}^{h-1}\left(\theta_{i}(\ell)^{\prime} b_{j}\right)^{2}}{\sum_{j=1}^{m} \sum_{\ell=0}^{h-1}\left(\theta_{i}(\ell)^{\prime} b_{j}\right)^{2}} . \]

The \(\mathrm{FE}_{i j}(h)\) lies in \([0,1]\) and varies across \(h\). Small values indicate that \(\varepsilon_{j t}\) contributes only a small amount to the variance of \(Y_{i t}\). Large values indicate that \(\varepsilon_{j t}\) contributes a major amount of the variance of \(\varepsilon_{i t}\). version.

A forecast error decomposition requires orthogonalized innovations. There is no non-orthogonalized

The forecast error decomposition can be calculated and displayed in Stata using the irf command. The command irf graph fevd produces graphs of the forecast error decomposition along with \(95 %\) asymptotic confidence intervals.

15.23 Identification of Recursive VARs

As we have discussed, a common method to orthogonalize the VAR errors is the lower triangular Cholesky decomposition which implies a recursive structure. The ordering of the variables is critical this recursive structure. Unless the errors are uncorrelated different orderings will lead to different impulse response functions and forecast error decompositions. The ordering must be selected by the user; there is no data-dependent choice.

In order for impulse responses and forecast error decompositions to be interpreted causally the orthogonalization must be identified by the user based on a structural economic argument. The choice is similar to the exclusion restrictions necessary for specification of an instrumental variables regression. By ordering the variables recursively we are effectively imposing exclusion restrictions. Recall that in our empirical example we used the ordering: (1) real GDP growth rate, (2) inflation rate, (3) Federal funds interest rate. This means that in the equation for GDP we excluded the contemporeneous inflation rate and interest rate, and in the equation for inflation we excluded the contemporenous interest rate. These are exclusion restrictions. Are they justified?

One approach is to order first the variables which are believed to be contemporaneously affected by the fewest number of shocks. One way of thinking about it is that they are the variables which are “most sticky” within a period. The variables listed last are those which are believed to be contemporanously affected by the greatest number of shocks. These are the ones which are able to respond within a single period to the shocks or are most flexible. In our example we listed output first, prices second and interest rates last. This is consistent with the view that output is effectively pre-determined (within a period) and does not (within a period) respond to price and interest rate movements. Prices are allowed to respond within a period in response to output changes but not in response to interest rate changes. The latter could be justified if interest rate changes affect investment decisions but the latter take at least one period to implement. By listing the federal funds rate last the model allows monetary policy to respond within a period to contemporeneous information about output and prices.

In general, this line of reasoning suggests that production measures should be listed first, goods prices second, and financial prices last. This reasoning is more credible when the time periods are short, and less credible for longer time periods. Further justifications for possible recursive orderings can include: (1) information delays; (2) implementation delays; (3) institutions; (4) market structure; (5) homogeneity; (6) imposing estimates from other sources. In most cases such arguments can be made but will be viewed as debatable and restrictive. In any situation it is best to be explicit about your choice and reasoning.

Returning to the empirical illustration it is fairly conventional to order the fed funds rate last. This allows the fed funds rate to respond to contemporeneous information about output and price growth and identifies the fed funds policy shock by the assumption that it does not have a contemporenous impact on the other variables. It is not clear, however, how to order the other two variables. For simplicity consider a traditional aggregate supply/aggregate demand model of the determination of output and the price level. If the aggregate supply curve is perfectly inelastic in the short run (one quarter) then output is effectively fixed (sticky) so changes in aggregate demand affect prices but not output. Changes in aggregate supply affect both output and prices. Thus we would want to order GDP first and inflation second. This choice would identify the GDP error as the aggregate supply shock. This is the ordering used in our example.

In contrast, suppose that the aggregate supply curve is perfectly elastic in the short run. Then prices are fixed and output is flexible. Changes in aggregate supply affect both price and output but changes in aggregate demand only affect output. In this case we would want to order inflation first and GDP second. This choice identifies the inflation error as the aggregate supply shock, the opposite case from the previous assumption!

If the choice between perfectly elastic and perfectly inelastic aggregate supply is not credible then the supply and demand shocks cannot be separately identified based on ordering alone. In this case the full set of impulse responses and error decompositions are not identified. However, a subset may be identified. In general, if the shocks can be ordered in groups then we can identify any shock for which a group has a single variable. In our example, consider the ordering (1) GDP and inflation; (2) federal funds rate. This means that the model assumes that GDP and inflation do not contemporeneously respond to interest rate movements but no other restrictions are imposed. In this case the fed funds policy shock is identified. This means that impulse responses of all three variables with respect to the policy shock are identified and similarly the forecast error composition of the effect of the fed funds shock on each variable is identified. These can be estimated by a VAR using the ordering (GDP, inflation, federal funds rate) as done in our example or using the ordering (inflation, GDP, federal funds rate). Both choices will lead to the same estimated impulse responses as described. The remaining impulse responses (responses to GDP and inflation shocks), however, will differ across these two orderings.

15.24 Oil Price Shocks

To further illustrate the identification of impulse response functions by recursive structural assumptions we repeat here some of the analysis from Kilian (2009). His paper concerns the identification of the factors affecting crude oil prices, in particular separating supply and demand shocks. The goal is to determine how oil prices respond to economic shocks and how the responses differ by the type of shock.

To answer this question Kilian uses a three-variable VAR with monthly measures of global oil production, global economic activity, and the global price of crude oil for \(1973 \mathrm{~m} 2-2007 \mathrm{~m} 12\). He uses global variables since the price of crude oil is globally determined. One innovation in the paper is that Kilian develops a new index of global economic activity based on ocean freight rates. His motivation is that shipping rates are directly related to the global demand for industrial commodities. This data set is posted on the textbook webpage as Kilian2009.

Kilian argues that these three variables are determined by three economic shocks: oil supply, aggregate demand, and oil demand. He suggests that oil supply shocks should be thought of as disruptions in production, processing, or shipping. Aggregate demand is global economic activity. Kilian also argues that oil demand shocks are primarily due to the precautionary demand for oil driven by uncertainty about future oil supply shortfalls.

To identify the shocks Kilian makes the following exclusion restrictions. First, he assumes that the short-run (one month) supply of crude oil is inelastic with respect to price. Equivalently, oil production takes at least one month to respond to price changes. This restriction is believed to be plausible because of technological factors in crude oil production. It is costly to open new oil fields; and it is nearly impossible to cap an oil well once tapped. Second, Kilian assumes that in the short-run (one month) global real economic activity does not respond to changes in oil prices (due to shocks specific to the oil market), while economic activity is allowed to respond to oil production shocks. This assumption is viewed by Kilian as plausible due to the sluggishness in the response of economic activity to price changes. Crude oil prices, however, are allowed to respond simultaneously to all three shocks.

Kilian’s identification strategy is similar to that described in the previous section for the simple aggregate demand/aggregate supply model. The separation of supply and demand shocks is achieved by exclusion restrictions which imply short-run inelasticities. The plausibility of these assumptions rests in part on the monthly frequency of the data. While it is plausible that oil production and economic activity may not respond within one month to price shocks, it is much less plausible that there is no response for a full quarter. Kilian’s least convincing identifying assumption (in my opinion) is the assumption that economic activity does not respond simultaneously to oil price changes. While much economic activity is pre-planned and hence sluggish to respond, some economic activity (recreational driving, for example) may immediately respond to price changes.

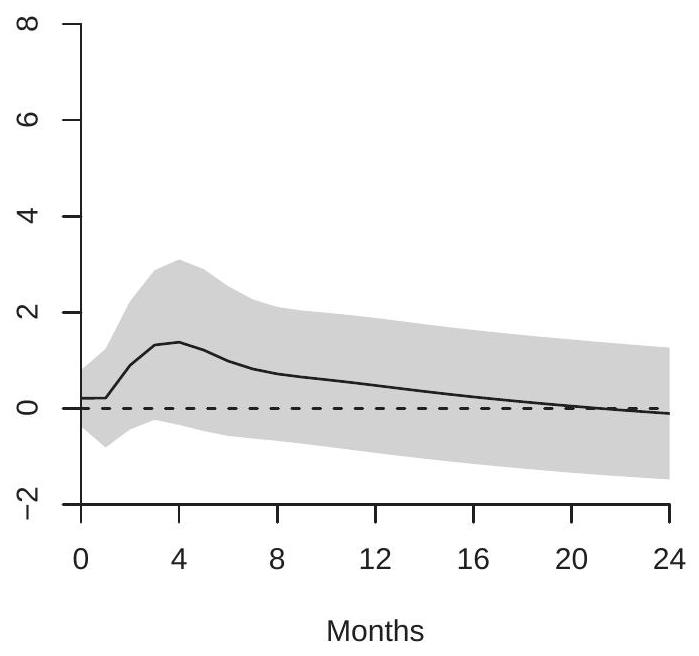

Kilian estimates the three-variable VAR using 24 lags and calculates the orthogonalized impulse response functions using the ordering implied by these assumptions. He does not discuss the choice of 24 lags but presumably this is intended to allow for flexible dynamic responses. If the AIC is used for model selection, three lags would be selected. For the analysis reported here I used 4 lags. The results are qualitatively similar to those obtained using 24 lags. For ease of interpretation oil supply is entered negatively (multiplied by -1) so that all three shocks are scaled to increase oil prices. Two impulse response functions for the price of crude oil are displayed in Figure \(15.2\) for 1-24 months. Panel (a) displays the response of crude oil prices due to an oil supply shock; panel (b) displays the response due to an aggregate demand shock. Notice that both figures have been displayed using the same y-axis scalings so that the figures are comparable.

What is noticeable about the figures is how differently crude oil prices respond to the two shocks. Panel (a) shows that oil prices are only minimally affected by oil production shocks. There is an estimated small short term increase in oil prices, but it is not statistically significant and it reverses within one year. In contrast, panel (b) shows that oil prices are significantly affected by aggregate demand shocks and the effect cumulatively increases over two years. Presumaby, this is because economic activity relies on crude oil and output growth is positively serially correlated.

The Kilian (2009) paper is an excellent example of how recursive orderings can be used to identify an orthogonalized VAR through a careful discussion of the causal system and the use of monthly observations.

15.25 Structural VARs

Recursive models do not allow for simultaneity between the elements of \(e_{t}\) and thus the variables \(Y_{t}\) cannot be contemporeneously endogenous. This is highly restrictive and may not credibly describe many economic systems. There is a general preference in the economics community for structural vector autoregressive models (SVARs) which use alternative identification restrictions which do not rely

- Supply Shock

.jpg)

- Aggregate Demand Schock

Figure 15.2: Response of Oil Prices to Orthogonalized Shocks

exclusively on recursiveness. Two popular categories of structural VAR models are those based on shortrun (contemporeneous) restrictions and those based on long-run (cumulative) restrictions. In this section we review SVARs based on short-run restrictions.

When we introduced methods to orthogonalize the VAR errors we pointed out that we can represent the relationship between the errors and shocks using either the equation \(e_{t}=\boldsymbol{B} \varepsilon_{t}\) (15.15) or the equation \(\boldsymbol{A} e_{t}=\varepsilon_{t}\) (15.17). Equation (15.15) writes the errors as a function of the shocks. Equation (15.17) writes the errors as a simultaneous system. A broader class of models can be captured by the equation system

\[ \boldsymbol{A} e_{t}=\boldsymbol{B} \varepsilon_{t} \]

where (in the \(3 \times 3\) case)

\[ \boldsymbol{A}=\left[\begin{array}{ccc} 1 & a_{12} & a_{13} \\ a_{21} & 1 & a_{23} \\ a_{31} & a_{32} & 1 \end{array}\right], \quad \boldsymbol{B}=\left[\begin{array}{lll} b_{11} & b_{12} & b_{13} \\ b_{21} & b_{22} & b_{23} \\ b_{31} & b_{32} & b_{33} \end{array}\right] . \]

(Note: This matrix \(\boldsymbol{A}\) has nothing to do with the regression coefficient matrix \(\boldsymbol{A}\). I apologize for the double use of \(\boldsymbol{A}\), but I use the notation (15.21) to be consistent with the notation elsewhere in the literature.)

Written out,

\[ \begin{aligned} &e_{1 t}=-a_{12} e_{2 t}-a_{13} e_{3 t}+b_{11} \varepsilon_{1 t}+b_{12} \varepsilon_{2 t}+b_{13} \varepsilon_{3 t} \\ &e_{2 t}=-a_{21} e_{1 t}-a_{23} e_{3 t}+b_{21} \varepsilon_{1 t}+b_{22} \varepsilon_{2 t}+b_{23} \varepsilon_{3 t} \\ &e_{3 t}=-a_{31} e_{1 t}-a_{32} e_{2 t}+b_{31} \varepsilon_{1 t}+b_{32} \varepsilon_{2 t}+b_{33} \varepsilon_{3 t} . \end{aligned} \]

The diagonal elements of the matrix \(\boldsymbol{A}\) are set to 1 as normalizations. This normalization allows the shocks \(\varepsilon_{i t}\) to have unit variance which is convenient for impulse response calculations.

The system as written is under-identified. In this three-equation example, the matrix \(\Sigma\) provides only six moments, but the above system has 15 free parameters! To achieve identification we need nine restrictions. In most applications, it is common to start with the restriction that for each common non-diagonal element of \(\boldsymbol{A}\) and \(\boldsymbol{B}\) at most one can be non-zero. That is, for any pair \(i \neq j\), either \(b_{j i}=0\) or \(a_{j i}=0\).

We will illustrate by using a simplified version of the model employed by Blanchard and Perotti (2002) who were interested in decomposing the effects of government spending and taxes on GDP. They proposed a three-variable system consisting of real government spending (net of transfers), real tax revenues (including transfer payments as negative taxes), and real GDP. All variables are measured in logs. They start with the restrictions \(a_{21}=a_{12}=b_{31}=b_{32}=b_{13}=b_{23}=0\), or

\[ \boldsymbol{A}=\left[\begin{array}{ccc} 1 & 0 & a_{13} \\ 0 & 1 & a_{23} \\ a_{31} & a_{32} & 1 \end{array}\right], \quad \boldsymbol{B}=\left[\begin{array}{ccc} b_{11} & b_{12} & 0 \\ b_{21} & b_{22} & 0 \\ 0 & 0 & b_{33} \end{array}\right] . \]

This is done so that that the relationship between the shocks \(\varepsilon_{1 t}\) and \(\varepsilon_{2 t}\) is treated as reduced-form but the coefficients in the \(\boldsymbol{A}\) matrix can be interpreted as contemporeneous elasticities between the variables. For example, \(a_{23}\) is the within-quarter elasticity of tax revenue with respect to GDP, \(a_{31}\) is the within-quarter elasticity of GDP with respect to government spending, etc.

We just described six restrictions while nine are required for identification. Blanchard and Perotti (2002) made a strong case for two additional restrictions. First, the within-quarter elasticity of government spending with respect to GDP is zero, \(a_{13}=0\). This is because government fiscal policy does not (and cannot) respond to news about GDP within the same quarter. Since the authors defined government spending as net of transfer payments there is no “automatic stabilizer” component of spending. Second, the within-quarter elasticity of tax revenue with respect to GDP can be estimated from existing microeconometric studies. The authors survey the available literature and set \(a_{23}=-2.08\). To fully identify the model we need one final restriction. The authors argue that there is no clear case for any specific restriction, and so impose a recursive \(\boldsymbol{B}\) matrix (setting \(b_{12}=0\) ) and experiment with the alternative \(b_{21}=0\), finding that the two specifications are near-equivalent since the two shocks are nearly uncorrelated. In summary the estimated model takes the form

\[ \boldsymbol{A}=\left[\begin{array}{ccc} 1 & 0 & 0 \\ 0 & 1 & -2.08 \\ a_{31} & a_{32} & 1 \end{array}\right], \quad \boldsymbol{B}=\left[\begin{array}{ccc} b_{11} & 0 & 0 \\ b_{21} & b_{22} & 0 \\ 0 & 0 & b_{33} \end{array}\right] . \]

Blanchard and Perotti (2002) make use of both matrices \(\boldsymbol{A}\) and \(\boldsymbol{B}\). Other authors use either the simpler structure \(\boldsymbol{A} e_{t}=\varepsilon_{t}\) or \(\boldsymbol{e}_{t}=\boldsymbol{B} \varepsilon_{t}\). In general, either of the two simpler structures are simpler to compute and interpret.

Taking the variance of the variables on each side of (15.21) we find

\[ \boldsymbol{A} \Sigma \boldsymbol{A}^{\prime}=\boldsymbol{B} B^{\prime} \text {. } \]

This is a system of quadratic equations in the free parameters. If the model is just identified it can be solved numerically to find the coefficients of \(\boldsymbol{A}\) and \(\boldsymbol{B}\) given \(\Sigma\). Similarly, given the least squares error covariance matrix \(\widehat{\Sigma}\) we can numerically solve for the coefficients of \(\widehat{\boldsymbol{A}}\) and \(\widehat{\boldsymbol{B}}\).

While most applications use just-identified models, if the model is over-identified (if there are fewer free parameters than estimated components of \(\Sigma\) ) then the coefficients of \(\widehat{\boldsymbol{A}}\) and \(\widehat{\boldsymbol{B}}\) can be found using minimum distance. The implementation in Stata uses MLE (which simultaneously estimates the VAR coefficients). The latter is appropriate when the model is correctly specified (including normality) but otherwise an unclear choice.

Given the parameter estimates the structural impulse response function is

\[ \widehat{\operatorname{SIRF}}(h)=\widehat{\Theta}(h) \widehat{\boldsymbol{A}}^{-1} \widehat{\boldsymbol{B}} . \]

The structural forecast error decompositions are calculated as before with \(b_{j}\) replaced by the \(j^{t h}\) column of \(\widehat{\boldsymbol{A}}^{-1} \widehat{\boldsymbol{B}}\)

The structural impulse responses are nonlinear functions of the VAR coefficient and covariance matrix estimators so by the delta method are asymptotically normal. Thus asymptotic standard errors can be calculated (using numerical derivatives if convenient). As for orthogonalized impulse responses the asymptotic normal approximation is unlikely to be a good approximation so bootstrap methods are an attractive alternative.

Structural VARs should be interpreted similarly to instrumental variable estimators. Their interpretation relies on valid exclusion restrictions which can only be justified by external information.

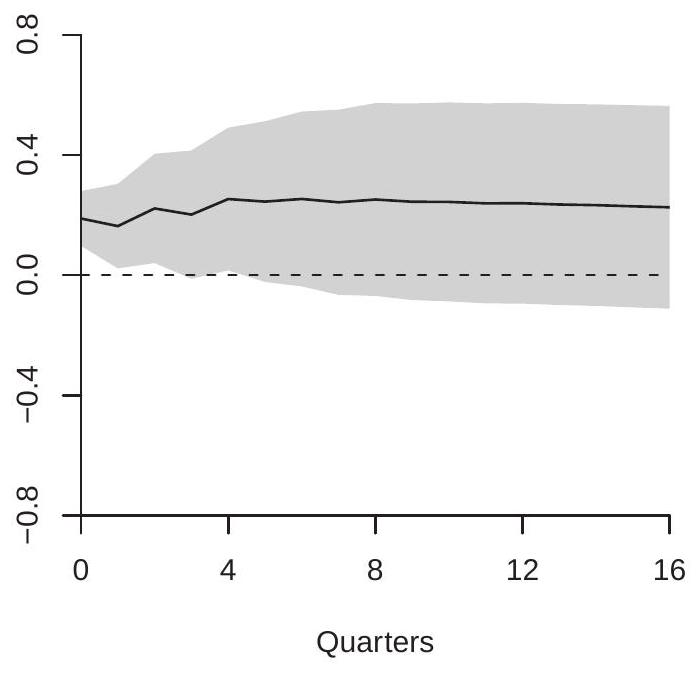

We replicate a simplified version of Blanchard-Perotti (2002). We use \({ }^{2}\) quarterly variables from FREDQD for 1959-2017: real GDP (gdpc1), real tax revenue (fgrecptx), and real government spending (gcec1), all in natural logarithms. Using the AIC for lag length selection we estimate VARs from one to eight lags and select a VAR(5). The model also includes a linear and quadratic function of time \({ }^{3}\). In Figure \(15.3\) we display the estimated structural impulse responses of GDP with respect to government spending (panel (a)) and tax shocks (panel (b)). The estimated impulse responses are similar to those reported by Blanchard-Perotti.

- Spending

.jpg)

- Taxes

Figure 15.3: Response of GDP to Government Spending and Tax Shocks

In panel (a) we see that the effect of a \(1 %\) government spending shock on GDP is positive, small (around \(0.2 %\) ), but persistent, remaining stable at \(0.2 %\) for four years. In panel (b) we see that the effect of a \(1 %\) tax revenue shock is quite different. The effect on GDP is negative and persistent, and more substantial than the effect of a spending shock, reaching about \(-0.5 %\) at six quarters. Together, the impulse response estimates show that changes in government spending and tax revenue have meaningful economic impacts. Increased spending has a positive effect on GDP while increased taxes has a negative effect.

\({ }^{2}\) These are similar to, but not the same as, the variables used by Blanchard and Perotti.

\({ }^{3}\) The authors detrend their data using a quadratic function of time. By the FWL Theorem this is equivalent to including a quadratic in time in the regression. The Blanchard-Perotti (2002) paper is an excellent example of how credible exclusion restrictions can be used to identify a non-recursive structural system to help answer an important economic question. The within-quarter exogeneity of government spending is compelling and the use of external information to fix the elasticity of tax revenue with respect to GDP is clever.